Michigan Medicaid Asset Protection Trusts & Testamentary Spousal SNTs

Key Takeaways

- Transferring assets into a MAPT triggers a 60-month Medicaid penalty clock, meaning it requires advance planning well before you actually need nursing home care.

- A Testamentary Spousal Special Needs Trust completely bypasses the devastating 5-year Medicaid look-back period for married couples.

- Because federal law mandates this trust must be created via a Last Will (and cannot be created via a Revocable Living Trust), the deceased spouse's estate becomes public record and incurs all standard probate court and executor fees.

Scenario: William and Margaret's Long-Term Care Dilemma

William and Margaret, a retired Grand Rapids couple, own a paid-off home and have spent decades building their savings. They are concerned that a future nursing home stay could force them to spend nearly everything they own before qualifying for Medicaid. Their challenge is finding a legal strategy that protects their assets without jeopardizing future eligibility for benefits.

For families like William and Margaret, basic planning tools are completely inadequate for long-term care protection. While revocable trusts avoid probate, they leave your life savings fully exposed to nursing home costs.

If you are facing the staggering expenses of aging in Michigan, you must deploy highly specific legal vehicles designed to shield your assets from the state. For comprehensive context on how these fit into your broader strategy, review our overview on Comprehensive Estate Planning Michigan: The Ultimate Guide to Types of Trusts. Let's explore the two most powerful tools available to Michigan seniors.

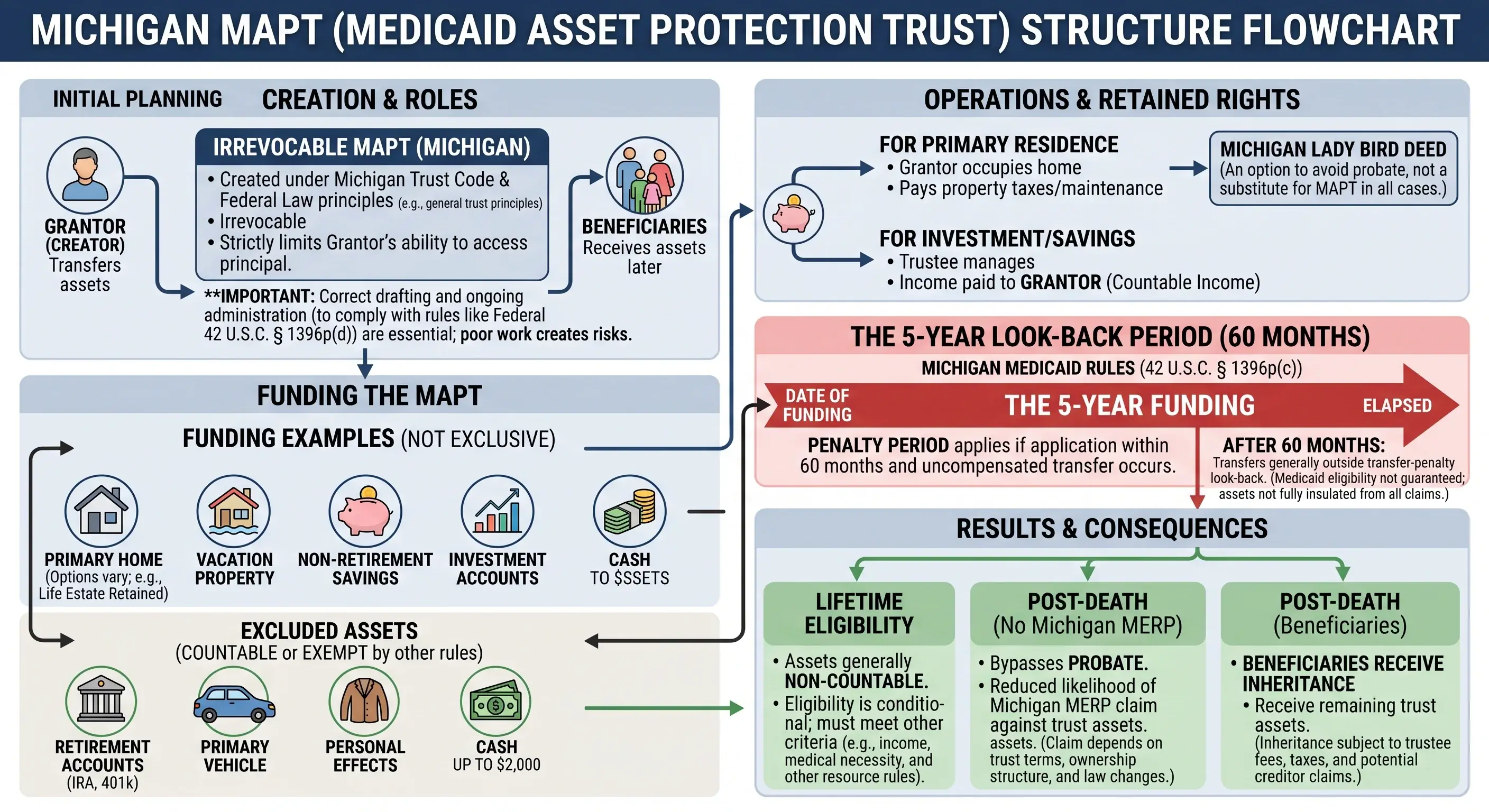

Understanding Michigan Medicaid Asset Protection Trusts (MAPTs)

A Medicaid Asset Protection Trust (MAPT) is an irrevocable trust specifically designed to hold assets to help a senior qualify for long-term care Medicaid in Michigan, while protecting those assets from the state.

The core mechanism of a MAPT involves legally removing assets from your personal ownership column so they are no longer counted by the Michigan Department of Health and Human Services (MDHHS). Achieving actual asset protection requires sophisticated, highly restrictive trust drafting well beyond standard estate planning.

Critical Distinction: MAPT vs. MDAPT

A MAPT is completely distinct from a Michigan Domestic Asset Protection Trust (MDAPT). An MDAPT is for general creditor protection and allows the settlor to access the principal. Retaining access to the principal would automatically disqualify you from Medicaid.

Lifetime Implications of a MAPT

When you establish a MAPT, you are trading immediate control for absolute future security.

- Once the 5-year Look-Back Period expires, the assets inside the trust are completely exempt from Medicaid asset limits.

- The settlor can retain the right to live in the home (via a Life Estate) and can continue to receive the income generated by the trust’s investments.

- You must completely surrender access to the trust's principal. If you suddenly need the principal to pay for living expenses, you cannot access it.

Scenario: The 5-Year Window for a Grand Rapids Family

William and Margaret transfer their Grand Rapids home into a MAPT in 2026. Because they transferred the asset, a 60-month penalty clock begins. If William needs nursing home care in 2029, the home is still exposed, and the transfer will trigger a penalty period of ineligibility. However, if he needs care in 2032, the house is completely protected, safely removed from their $9,950 countable asset limit, and preserved for their children.

Postmortem Benefits and Risks

After you pass away, the MAPT continues to provide significant advantages to your heirs, provided it was managed correctly. Proactive planning heavily mitigates post-death bureaucratic nightmares.

- The trust completely avoids the Michigan Department of Health and Human Services Estate Recovery Program because the assets belong to the trust, not the deceased’s probate estate.

- The assets pass directly to your heirs without probate delay, and the heirs still receive a full "step-up" in basis on highly appreciated assets like real estate.

- The trust administration requires formal wrap-up steps.

- If the trust was poorly drafted or managed incorrectly during life (e.g., the grantor secretly accessed the principal), the state may challenge the trust and attempt to place a lien on the property after death.

MCL 400.112gThe department of community health shall establish and operate the Michigan medicaid estate recovery program to comply with requirements contained in section 1917 of title XIX... Actions necessary to collect amounts subject to estate recovery for medical services...

The Testamentary Spousal Special Needs Trust

While MAPTs require a strict five-year waiting period, married couples have access to a distinct statutory exception. A Testamentary Spousal Special Needs Trust is a highly specific, statutorily protected Medicaid exception in Michigan (and federally) where a healthy spouse creates a trust explicitly within their Last Will and Testament for the benefit of a disabled surviving spouse.

Unlike standard first-party or third-party disability trusts—which you can read about in Michigan Special Needs Trusts: The Core Framework for Protecting SSI and Medicaid—this vehicle is structurally dependent on the marital relationship and must go through probate court.

Lifetime Implications for the Healthy Spouse

- The trust exists entirely as a dormant provision in a Last Will, meaning there are absolutely zero lifetime restrictions, tax consequences, or funding hassles for the healthy spouse while they are alive.

- It offers absolutely zero asset protection for the healthy spouse if the healthy spouse is the one who ends up needing long-term care or nursing home Medicaid first.

Postmortem Implications: The Spousal Loophole

When the healthy spouse passes away, this trust springs into action, serving as the ultimate Medicaid spousal loophole.

- When the healthy spouse dies, the probate estate funds the trust, and the disabled surviving spouse can instantly qualify for Michigan Medicaid without any transfer penalty periods, preserving the deceased's wealth to supplement the survivor's care.

- The trust is statutorily guaranteed to go through the Michigan Probate Court.

Strategic Execution

Navigating the exact intersection of federal exemptions under 42 U.S.C. § 1396p(d)(2)(A) and Michigan's local probate courts requires absolute precision.

To understand how the necessary probate fees may impact the estate, families can utilize our Michigan Probate Cost Calculator to evaluate the trade-offs of this strategy.

If you are looking to take the next step in planning for your loved ones, please contact us today to schedule a consultation and secure your future.